Private Education Loans

After exhausting federal financial aid options, if you need additional funding, you may decide to look into private education loans. A private education loan, also known as an alternative loan, is a loan issued by a lender such as a bank or credit union. These loans are primarily used to supplement federal programs when federal aid and scholarships do not meet the cost of attendance.

90% of lenders in the U.S. use FICO scores when determining if a student is approved or denied for a private loan. FICO scores are based on a snapshot of credit behavior at that given time and are subject to change. Most lenders use your FICO score to determine if you will be able to re-pay the loan by looking at your debt to income ratio, they often look at income as well, and use the FICO score to determine your interest rate.

If you do not have established credit or a high enough FICO score to qualify for a loan, you may need a credit worthy co-signer to co-sign the loan you are applying for. You are able to proactively use a co-signer when you first complete the application, or if you’d like to be evaluated first, you can, and then add a co-signer if denied. If you’re looking to improve your financial health, here are some tips:

- Pay bills on time.

- Keep credit balances as low as possible.

- Pay more on your credit card and loans than the monthly minimum.

- Check your credit report frequently – utilize free tools, most banks offer a free credit check!

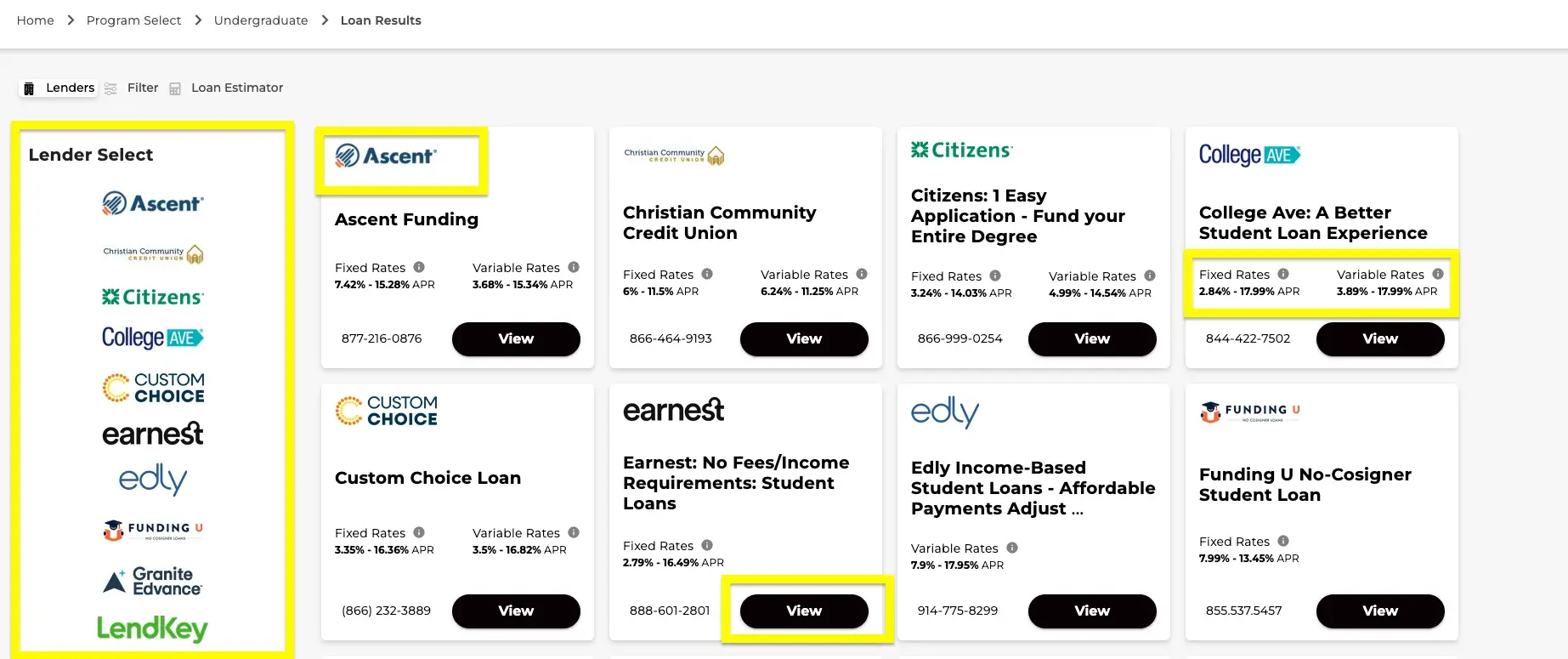

Elm Select

There’s a large market for private loans. To find the best loan(s) for you, we recommend using Elm Select., a free tool that allows borrowers to search among the most commonly used sources of private education loans. It’s not a comprehensive list, but includes many of the primary private loan lenders. Here's how to use Elm Select:

- Select “Azusa Pacific University” as your school and select your program (APU accepts only Undergraduate, Graduate, and Parent Loans).

- Once you select your program, click “View Loans!”

- Below is a snapshot of the results page, where you can see which loans are being offered and the available interest rates.

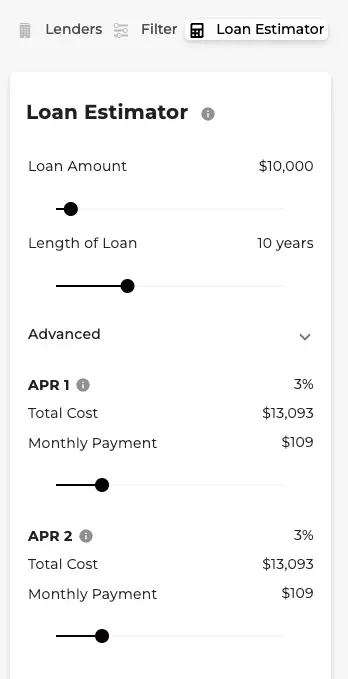

It also has a “Loan Estimator” tool to estimate what your repayment will look like based on the amount you borrow:

Once you determine which loan you’d like to apply for, you can click through to that lender’s website to begin the application. That is where your credit will be reviewed, and if approved, you’ll be granted the loan. The lender will then send the information to APU; once it’s received, we'll add it to your financial aid package.

Juno

Juno organizes large groups of students to negotiate better loan terms and potentially lower interest rates with private lenders. To begin exploring loan options, borrowers complete a brief questionnaire with no impact on their credit score.

The lender identified by Juno agree to provide members with options, which may include terms more competitive than what students could secure on their own, and there’s no obligation to accept the loans offered. Note: The listing on Juno represents lenders who have negotiated specific terms for their members and is not inclusive of all private loan lenders available to students.

Juno also provides free 1:1 guidance to thousands of borrowers each year, helping them compare their options with confidence.

Visit the Juno website or schedule time with a Juno advisor

Disclaimer: Azusa Pacific University does not sponsor Juno, and students have no obligation to utilize Juno's services. APU is providing information about these services strictly as an independent resource so students can evaluate all options for funding their education. These links are provided solely as a courtesy.

Note: Federal Direct Loans generally have more favorable terms and conditions (PDF) than private loans. We recommend that you utilize all federal aid eligibility before turning to private loans.

Note that Azusa Pacific University does not recommend a specific lender or lenders; this list is offered as a way for students to compare their private lending options. Employees responsible for processing loans adhere to a strict student loan Code of Conduct.